- Author

-

Kym Eaton

Kym Eaton

Running a hospitality business in Australia is no easy feat, and understanding the ins and outs of payment processing can feel like a whole other challenge.

Whether you're opening your first café or managing an established restaurant group, getting payment processing right is crucial for cash flow, customer satisfaction, and operational efficiency.

According to the Reserve Bank of Australia, electronic payments now account for over 93% of all point-of-sale transactions in hospitality, up from 78% pre-pandemic. Fast, reliable payment processing isn't optional anymore, it's essential for business survival.

This FAQ guide answers the 8 most common questions we hear from Australian hospitality operators about payment processing. You'll learn how the system works, what it costs, how to integrate it with your POS, and what to watch out for when choosing a provider.

Whether you're a seasoned restaurateur or just starting out, this guide will help you make informed decisions about payment processing, ensuring smooth transactions, happy customers, and a thriving business.

Quick Answers - Payment Processing Essentials

What it costs: 1.5-3.5% per transaction + 20-30¢ fixed fee (varies by provider and card type)

Best pricing model: Interchange-plus (most transparent for Australian hospitality)

Settlement time: 2-3 business days (some providers offer next-day)

Must-have features: PCI DSS compliance, POS integration, Australian-based support

How integration works: Payment terminal communicates directly with POS for automatic data sync

Security standard: PCI Level 1 certification with end-to-end encryption

Biggest mistake: Choosing embedded payment processing that locks you into one provider

Ready to choose a payment processor? Check out the payment providers that PowerEPOS integrates with.

1. How does payment processing work for restaurants and cafés?

💡 Quick Answer:

Payment processing is the system that securely transfers money from a customer's account to your business bank account when they pay with a card or digital wallet. The process involves the customer's bank, card networks (Visa, Mastercard, Eftpos), and your payment processor working together to approve transactions and settle funds, typically within 2-3 business days.

The payment processing system involves multiple parties working together to move money safely and quickly.

The Key Players:

Customer's Issuing Bank

The bank that issued the customer's card (e.g., ANZ, Commonwealth Bank, NAB)

Card Network

Visa, Mastercard, American Express, or Eftpos, the network that routes the transaction

Acquiring Bank/Processor

Your payment provider (like Tyro, Zeller, or your bank) that processes transactions and deposits funds

Your Business Bank Account

Where the money ultimately lands after settlement

How a Transaction Flows:

- Customer taps/inserts card at your venue

- Card details encrypted and sent to card network

- Card network contacts customer's bank to verify funds

- Bank approves or declines transaction (happens in 2-5 seconds)

- Approval sent back through network to your terminal

- Transaction batched with others at end of day

- Funds settled to your account (2-3 business days later)

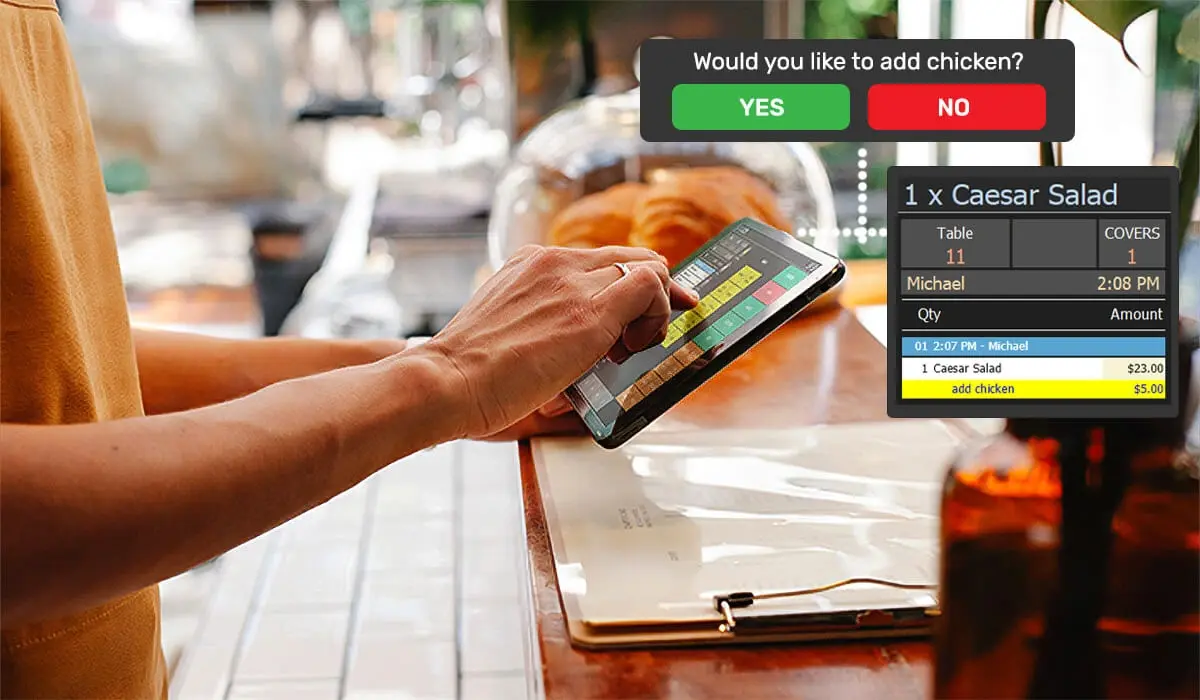

All of this happens automatically through your POS system and payment terminal. The seamless integration between these systems is what makes modern hospitality payment processing fast and reliable.

💡 Triniteq Tip: PowerEPOS integrates directly with 15+ payment processors, so transaction data flows automatically into your sales reports, inventory tracking, and accounting, no manual reconciliation needed.

2. Why is payment processing important for my hospitality business?

💡 Quick Answer:

Payment processing directly impacts three critical business areas: cash flow (faster settlement = better working capital), customer experience (fast checkout keeps queues moving), and operational efficiency (automated reconciliation saves hours weekly). The right system can save thousands annually in fees while improving service quality.

Modern payment processing is essential infrastructure for hospitality businesses. Here's why it matters:

Cash Flow Management

Fast settlement times improve your ability to manage daily expenses:

- Next-day settlement helps with inventory purchasing and staff wages

- Predictable deposit schedules make financial planning easier

- Reduced working capital needs when money isn't stuck in transit for days

A restaurant processing $50,000 monthly with 2-day settlement has $3,300 constantly "in transit." Next-day settlement cuts this to $1,650, that's $1,650 more available working capital.

Customer Experience

Payment processing speed directly affects customer satisfaction:

- Contactless transactions complete in under 5 seconds

- Multiple payment options meet modern customer expectations

- Fast checkout reduces queue times during busy periods

A 2024 study found that hospitality venues offering 4+ payment methods saw 18% higher transaction values compared to cash-only or limited-option venues.

Operational Efficiency

Integrated payment processing simplifies back-office operations:

- Automatic reconciliation eliminates manual end-of-day counting

- Real-time reporting helps track sales and identify trends instantly

- Reduced errors from automatic data syncing between POS and payment systems

- Simplified accounting with all transaction data in one system

Risk Management

Secure payment processing protects your business:

- PCI-compliant processing shields you from data breach liability

- Fraud detection tools prevent unauthorised transactions

- Clear chargeback processes minimise financial disputes

- Encrypted data transmission protects customer information

Choosing the right payment processing solution helps you get paid faster, improve customer satisfaction, and streamline operations,all of which directly impact your profitability.

3. What payment methods should I offer at my hospitality venue?

💡 Quick Answer:

Modern Australian customers expect debit/credit cards, mobile wallets (Apple Pay, Google Pay), and contactless tap-and-go as standard. Venues offering 4+ payment methods see 18% higher transaction values. Consider adding Buy Now Pay Later (Afterpay, Zip) for higher-end venues or large group bookings.

Offering the right mix of payment methods meets customer expectations and can increase revenue.

Essential Payment Methods for Australian Hospitality:

Debit and Credit Cards

- Eftpos debit: Lowest processing fees (0.5-1.0%)

- Visa/Mastercard credit: Standard fees (1.5-2.5%)

- American Express: Higher fees (2.5-3.5%) but some customers prefer it

Mobile Wallets

- Apple Pay: Very popular with iPhone users in metro areas

- Google Pay: Standard for Android users

- Samsung Pay: Growing adoption

Mobile wallet transactions process exactly like card payments, no extra fees for merchants. The customer just taps their phone instead of their card.

Contactless Payments

- "Tap and go" is now the standard expectation in Australian hospitality

- Customers expect contactless for all transactions under $200

- Faster than chip-and-PIN, which reduces queue times during busy periods

Buy Now Pay Later (BNPL) - Optional but Growing

- Afterpay, Zip, and similar services gaining popularity

- Higher transaction fees (3-6%) but can increase average order value

- Best for: Fine dining, group bookings, higher-ticket items

- Popular with: 25-40 year old demographics

Cash - Declining But Not Dead

- Less than 10% of hospitality transactions in Australian metro areas

- Still important for some customers

- Consider cash handling costs vs. card processing fees

What About Cryptocurrency?

Currently very limited adoption in Australian hospitality. Most venues can skip this for now unless you have a specific tech-savvy customer base requesting it.

Recommendation by Venue Type:

| Venue Type | Must Have | Should Consider | Can Skip |

|---|---|---|---|

| Quick Service Café | Cards, contactless, mobile wallets | BNPL for catering orders | Cash-only option |

| Casual Dining | Cards, contactless, mobile wallets | BNPL for large groups | Cryptocurrency |

| Fine Dining | All cards including Amex, mobile wallets | BNPL (increases large bookings) | Cash priority |

| Pubs/Bars | Cards, contactless, mobile wallets | BNPL for functions | Cash-only |

💡 Triniteq Integration: PowerEPOS supports all major Australian payment methods through integrations with Zero Payments, Tyro, Zeller, all major banks, and 15+ other providers. Your payment terminal handles the payment types, your POS handles the transaction recording. See our payment integration options →

Pricing & Fees

4. What are the different types of payment processing pricing models?

💡 Quick Answer:

Three main models: Flat-rate (simple but expensive at scale), Interchange-plus (transparent and fair), and Tiered (avoid, opaque and deceptive). For Australian hospitality venues processing $10,000+ monthly, interchange-plus offers the best value and transparency.

Understanding pricing models helps you avoid overpaying. Here's how each works:

Payment Processing Pricing Models Comparison

| Model | How It Works | Example | Best For | Pros | Cons |

|---|---|---|---|---|---|

| Flat-Rate | Fixed % per transaction | 2.5% + 30¢ every transaction | Very small cafés (< $5k/month) | Simple, predictable | Expensive at higher volumes |

| Interchange-Plus ⭐ | Actual cost + markup | 1.5% interchange + 0.5% markup | Most venues ($5k+ monthly) | Transparent, fair, scales well | Monthly cost varies slightly |

| Tiered | Qualified/mid/non-qualified rates | Advertised "1.5%" but most pay 3%+ | ❌ Avoid this model | None for merchants | Opaque, deceptive, expensive |

Flat-Rate Pricing

How it works: Every transaction costs the same percentage regardless of card type.

Example: 2.5% + 30¢ whether customer uses low-cost Eftpos debit or expensive American Express.

Pros:

- Very simple to understand

- Completely predictable monthly costs

- No surprises on your statement

Cons:

- You overpay on low-cost transactions (Eftpos debit)

- Provider keeps the savings when customers use cheaper cards

- Becomes very expensive as volume increases

Best for: Brand new cafés processing under $5,000 monthly who value simplicity over savings.

Interchange-Plus Pricing ⭐ RECOMMENDED

How it works: You pay the actual interchange rate (set by card networks) plus a fixed processor markup.

Example:

- Eftpos debit (0.5% interchange) + 0.5% markup = 1.0% total

- Visa credit (1.5% interchange) + 0.5% markup = 2.0% total

- Amex (2.5% interchange) + 0.5% markup = 3.0% total

Pros:

- Complete transparency, you see exactly what you're paying

- Fairest pricing model available

- As your volume grows, costs scale efficiently

- Easy to compare providers (just compare the markup)

Cons:

- Monthly costs vary slightly based on your customer payment mix

- Requires understanding two components (interchange + markup)

Best for: Most hospitality venues processing $5,000+ monthly. The transparency and savings outweigh the minimal complexity.

Tiered Pricing ❌ AVOID

How it works: Processors categorise transactions into "qualified," "mid-qualified," and "non-qualified" tiers with different rates.

Example: Advertised as "1.5%" but processors push most transactions into higher tiers (2.5-3.5%+).

Pros: None for merchants.

Cons:

- Intentionally opaque, you can't see actual costs

- Processors control which tier each transaction falls into

- No way to verify you're being charged fairly

- Almost always more expensive than interchange-plus

Best for: Nobody. This model benefits processors at the expense of merchants.

Which Model Should You Choose?

Processing under $5,000/month:

Flat-rate is acceptable for simplicity, but still compare interchange-plus quotes.

Processing $5,000-$50,000/month:

Interchange-plus is almost always cheaper and worth the minimal complexity.

Processing $50,000+/month:

Interchange-plus is essential. You should also negotiate your markup rate down.

Never choose tiered pricing. If a provider only offers tiered pricing, choose a different provider.

Need help comparing pricing models for your venue? [Read our complete payment processor selection guide with cost calculators →]

5. What are payment processing fees for hospitality businesses in Australia?

💡 Quick Answer:

Total fees typically range from 1.0-3.5% per transaction. Eftpos debit is cheapest (0.5-1.0%), Visa/Mastercard credit costs 1.5-2.5%, and American Express is most expensive (2.5-3.5%). Fees have three components: interchange rate (set by card networks), processor markup (negotiable), and miscellaneous fees (terminals, PCI compliance, etc.).

Payment processing fees have multiple components. Understanding each helps you evaluate true costs.

Fee Component Breakdown:

1. Wholesale Rate (Interchange Fee)

What it is: Base fee set by card networks and issuing banks

Who controls it: Visa, Mastercard, Eftpos, Amex, not your processor

Can you negotiate it? No, it's the same for everyone

Typical Australian Interchange Rates:

- Eftpos debit: 0.5-0.8%

- Visa/Mastercard debit: 0.8-1.0%

- Visa/Mastercard credit: 1.3-1.8%

- Premium credit cards: 1.8-2.2%

- American Express: 2.0-3.0%

2. Processor Markup

What it is: Fee your payment provider adds on top of interchange

Who controls it: Your processor (Tyro, Zeller, your bank, etc.)

Can you negotiate it? Yes, especially with higher volumes

Typical Markup Rates:

- Standard: 0.5-0.8% + 10-30¢ per transaction

- Negotiated (high volume): 0.3-0.5% + 10-15¢ per transaction

3. Miscellaneous Fees

Monthly/Fixed Fees:

- Terminal rental: $0-50/month (or buy outright for $300-600)

- PCI compliance: $0-30/month (some providers include it)

- Payment gateway (for online orders): $10-30/month

- Monthly account fee: $0-30/month

Per-Incident Fees:

- Chargeback fee: $15-25 per disputed transaction

- Failed transaction fee: $0-1 per failed attempt

Real-World Example: $100 Restaurant Bill

Customer pays with Visa Credit:

| Fee Component | Rate | Amount |

|---|---|---|

| Interchange fee | 1.5% | $1.50 |

| Processor markup | 0.5% + 20¢ | $0.70 |

| Total cost | 2.2% | $2.20 |

| You receive | $97.80 |

Customer pays with Eftpos Debit:

| Fee Component | Rate | Amount |

|---|---|---|

| Interchange fee | 0.6% | $0.60 |

| Processor markup | 0.5% + 20¢ | $0.70 |

| Total cost | 1.3% | $1.30 |

| You receive | $98.70 |

The difference? You keep $0.90 more when customers use Eftpos debit instead of credit.

Australian Surcharging Rules:

You can legally pass card processing costs to customers in Australia, but:

- Surcharges must not exceed your actual cost of acceptance

- You must display surcharge amounts clearly before payment

- ACCC monitors excessive surcharging

Typical surcharge amounts:

- Eftpos debit: 0.5-1.0%

- Visa/Mastercard credit: 1.5-2.0%

- American Express: 2.5-3.5%

Monthly Cost Estimate:

Small Café ($10,000/month card sales):

- Average rate: 1.8%

- Transaction fees: ~$180/month

- Miscellaneous fees: ~$20/month

- Total: ~$200/month

Medium Restaurant ($50,000/month card sales):

- Average rate: 1.7% (negotiated)

- Transaction fees: ~$850/month

- Miscellaneous fees: ~$30/month

- Total: ~$880/month

Large Venue ($100,000/month card sales):

- Average rate: 1.5% (negotiated)

- Transaction fees: ~$1,500/month

- Miscellaneous fees: ~$50/month

- Total: ~$1,550/month

💡 Cost-Saving Tip: Because PowerEPOS integrates with 15+ payment processors and charges zero transaction fees itself, our customers can shop competitively and negotiate better rates. Some hospitality customers have reduced payment processing costs by 30-40% just by switching providers, without changing their POS system.

6. Can restaurants negotiate payment processing fees?

💡 Quick Answer:

Yes, the processor markup and miscellaneous fees are negotiable, especially if you process $50,000+ monthly or have multiple locations. The interchange fee (set by card networks) is non-negotiable. Getting competitive quotes from 2-3 providers is the most effective negotiation tactic.

You have more negotiating power than you might think.

What You CAN Negotiate: ✅

Processor Markup

- Standard markup: 0.5-0.8%

- With negotiation: 0.3-0.5%

- Savings on $50k monthly: $100-250/month

Per-Transaction Fee

- Standard: 20-30¢

- With negotiation: 10-15¢

- Savings (200 transactions/day): $600-1,200/month

Monthly/Miscellaneous Fees

- Terminal rental (often waivable)

- PCI compliance fees (can be included in package)

- Statement fees, account fees

What You CANNOT Negotiate: ❌

Interchange Fee

- Set by Visa, Mastercard, Eftpos, American Express

- Same rate for all merchants regardless of size

- Non-negotiable even with millions in volume

Negotiation Leverage Points:

High Volume

- Processing $50,000+/month: 0.2-0.3% reduction possible

- Processing $100,000+/month: 0.3-0.5% reduction possible

- Industry data: Venues in this range can save $1,200-$3,000 annually

Multi-Location Groups

- Combine volume across all venues for group pricing

- Enterprise rates available for 3+ locations

- Dedicated account manager often included

Long Transaction History

- 12+ months of reliable processing

- Low chargeback rates strengthen position

- Consistent volume month-over-month

Competitive Quotes ⭐ Most Effective

- Get quotes from 2-3 providers

- Processors often match or beat competitor rates

- Shows you're serious about switching if needed

Example:

Brisbane Restaurant Group (3 Locations)

- Current processor: 2.4% average rate

- Monthly volume: $150,000 combined

- Monthly cost: $3,600

After negotiation:

- New provider: 1.7% average rate

- Same volume: $150,000

- New monthly cost: $2,550

- Savings: $1,050/month = $12,600/year

Switching time: 4 hours across all 3 venues with PowerEPOS

💡 Pro Tip: Switching providers is often more effective than renegotiating with your current one. Processors know that most merchants won't switch (either locked in by contracts or embedded POS systems). With PowerEPOS's open integration, you can switch in a day, which gives you real negotiating power.

Technical Integration

7. What is embedded payment processing and should I avoid it?

💡 Quick Answer:

Embedded payment processing is when your POS provider locks you into using only their payment processor. While convenient initially, it prevents you from negotiating better rates, makes switching expensive, and costs thousands extra annually. Choose a POS with open payment integrations for long-term flexibility and savings.

Embedded payment processing is one of the most expensive hidden costs in hospitality technology.

How Embedded Processing Works:

Some POS providers build payment processing directly into their system:

- You can ONLY use their payment processor

- Switching processors means replacing your entire POS

- You can't negotiate rates (they know you're locked in)

- Transaction fees are often higher than market rates

Examples:

- Square (can only use Square payments)

- Toast (strongly pushes Toast payments)

- Some "all-in-one" cloud POS systems

Why POS Companies Push It:

For them:

- They earn commission on every transaction you process

- On a $50,000/month venue, they earn $500-1,000/month

- It's a profit center disguised as "convenience"

- Locks you into their ecosystem

For you initially:

- Convenient (one provider for everything)

- Simple setup (one call, one contract)

For you long-term:

- Expensive (rates creep up, you can't leave)

- No negotiating leverage

- Switching costs are prohibitive

The Hidden Cost:

Example: Restaurant Processing $50,000/Month

| Provider Type | Rate | Monthly Cost | Annual Cost | 5-Year Cost |

|---|---|---|---|---|

| Embedded (locked) | 2.5% | $1,250 | $15,000 | $75,000 |

| Open integration (negotiated) | 1.8% | $900 | $10,800 | $54,000 |

| Difference | 0.7% | $350 | $4,200 | $21,000 |

Over 5 years, embedded processing costs $21,000 extra just because you couldn't switch providers.

What Happens When:

Rates Increase:

- Embedded: You're stuck paying higher rates or replacing entire POS

- Open: Switch to cheaper provider in a day

Service Declines:

- Embedded: Accept poor service or expensive POS replacement

- Open: Move to provider with better support

You Want to Negotiate:

- Embedded: No leverage (provider knows you can't leave easily)

- Open: Use competitor quotes to negotiate better rates

Your Business Grows:

- Embedded: No volume discounts (you can't shop around)

- Open: Renegotiate based on higher volume or switch to enterprise provider

✅ PowerEPOS Approach - Open Payment Integration:

PowerEPOS integrates with 15+ payment processors, giving you complete freedom:

Choose Your Provider:

- Zero Payments for great rates

- Tyro for hospitality-focused support

- Zeller for next-day settlement and low fees

- Bank processors for relationship pricing

- Compare and choose what's best for YOUR business

Switch When It Makes Sense:

- Provider raises rates? Switch to competitor

- Service quality drops? Move to better option

- Change processors in 1-2 hours

- No POS disruption, no data loss

Negotiate Better Rates:

- Providers know you can switch easily

- Use competitor quotes for leverage

- Renegotiate annually based on volume

- Real negotiating power

Example:

Melbourne Café - Before PowerEPOS:

- Locked into POS provider's payment processor

- Paying 2.6% effective rate

- Processing $25,000/month

- Monthly cost: $650

After Switching to PowerEPOS:

- Switched to Zeller at negotiated 1.9% rate

- Same volume: $25,000/month

- New monthly cost: $475

- Savings: $175/month = $2,100/year

- Switching time: 2 hours

- Kept all menu data, settings, history

How to Identify Embedded Processing:

Red Flags:

- "All-in-one POS and payments package"

- "Payments included in your monthly subscription"

- Can't use other payment processors

- Payment processing fees go to POS provider

Questions to Ask:

- "Can I use my own payment processor?"

- "What happens if I want to switch processors?"

- "Who receives the transaction fees?"

- "What integrations do you support?"

If answers are vague or restrictive, it's embedded processing.

💡 Bottom Line: Embedded payment processing might seem convenient, but it costs thousands in lost negotiating power and higher fees over time. Choose a POS with open integrations from day one.

8. How do I integrate payment processing with my POS system?

💡 Quick Answer:

Choose a payment processor with certified integration to your POS. This enables automatic transaction syncing, simplified checkout, reduced errors, and unified reporting. With PowerEPOS, integration setup takes 1-2 hours and supports 15+ processors for maximum flexibility.

Integrated payment processing is essential for modern hospitality operations.

Why Integration Matters:

Operational Benefits:

- Transaction amounts sync automatically from POS to terminal

- No manual entry of sale totals

- Payment confirmation flows back to POS instantly

- Single receipt prints with complete transaction details

- Automatic end-of-day reconciliation

Accuracy Benefits:

- Eliminates manual entry errors

- Automatic calculation of surcharges, tips, taxes

- Payment records match POS records perfectly

- Simplified accounting and bookkeeping

Speed Benefits:

- Checkout process 30-40% faster than non-integrated systems

- Customer sees total, taps card, receipt prints, done

- Reduced queue times during busy periods

Reporting Benefits:

- Real-time sales and payment data in one dashboard

- Payment method breakdown (card types, mobile wallet usage)

- Settlement tracking and reconciliation

- No manual spreadsheet reconciliation needed

How POS-Payment Integration Works:

Step-by-Step Transaction Flow:

- Staff enters order in POS: $85.50

- POS calculates surcharge (if applicable): +$2.14 (2.5% for Amex)

- POS sends total to payment terminal: $87.64

- Terminal displays amount to customer

- Customer taps/inserts card

- Terminal processes payment, returns approval to POS

- POS marks order as paid, updates all reports

- Receipt prints with itemised order + payment details

Total time: 5-10 seconds from "send to payment" to receipt printing.

What "Certified Integration" Means:

Official Partnership:

- POS provider and payment processor have tested integration

- Supported by both companies

- Regular updates maintain compatibility

Technical Requirements:

- Real-time communication between POS and terminal

- Secure encrypted data transmission

- Automatic error handling

Support Benefits:

- Both providers support the integration

- Clear troubleshooting procedures

- Documentation and training materials

Key Features to Look For:

Offline Capability ✅

- POS and payments work during internet outages

- Transactions stored locally and synced when connection returns

- Critical for avoiding lost sales

Real-Time Communication ✅

- Approval/decline happens in under 5 seconds

- No delays between payment and receipt

- Immediate transaction confirmation

Comprehensive Data Sync ✅

- Card type captured (Visa, Mastercard, Eftpos, Amex)

- Payment method (chip, contactless, mobile wallet)

- Transaction IDs for chargeback management

- Tip amounts, surcharges

Multiple Terminal Support ✅

- Support for 2+ terminals at busy venues

- Each terminal syncs with POS independently

- Staff can process payments from any terminal

PowerEPOS Payment Integration Advantages:

15+ Integrated Processors:

- Tyro, Zeller, ANZ, NAB, Westpac, CBA

- All with certified integrations

Easy Switching:

- Change processors without POS disruption

- Update settings in minutes

- Test and go live fast

- No staff retraining needed (process stays the same)

Unified Reporting:

- In-venue and online payments in one dashboard

- Real-time settlement tracking

- Payment method breakdown

- Automatic reconciliation

💡 Integration Tip: Test your payment integration during a quiet period before going live during busy service. Process a few transactions, void one, process a refund, make sure all scenarios work smoothly before peak hours.

Takeaways

Payment processing is essential infrastructure for modern Australian hospitality businesses. Understanding how it works, what it costs, and how to integrate it properly helps you make informed decisions that impact your cash flow, customer experience, and operational efficiency.

Payment Processing for Australian Hospitality 2026: The Complete Guide

FAQs About Payment Processing

If you're seeking a quality, Australian-made and supported Point of Sale solution for your hospitality or retail business, look no further than Triniteq.

Our innovative technologies and high-quality service are designed to simplify operations, enhance customer experience, and make you more money.

Discover our range of products and services today.

If you're new to Triniteq and PowerEPOS, our new cloud-hybrid POS system, contact us for more info.

Related articles

A few weeks ago, I was catching up with some of our customers and the conversations kept ...

Switching payment processors should be one of the simplest cost-saving decisions a ...

If you're shopping for a POS system for your restaurant, cafe, bar, or hospitality venue, ...